India's AI-powered Enterprise Content Management platform. 4 native AI features. Start your free trial →

audit-ready DMS11 min read8 July 2025

Document Management for Banks: Compliance, Audit, and Beyond

Document management for banks with stronger compliance, audit readiness, secure access, and better control over financial records. Document Management for Banks: Compliance, Audit, and Beyond Document…

Banks don’t just “store documents.” They manage regulated evidence. Every account opening form, KYC artifact, loan file, sanction screening record, customer communication, vendor contract, board policy, audit response, and exception note can become a compliance artifact—often years after it was created.

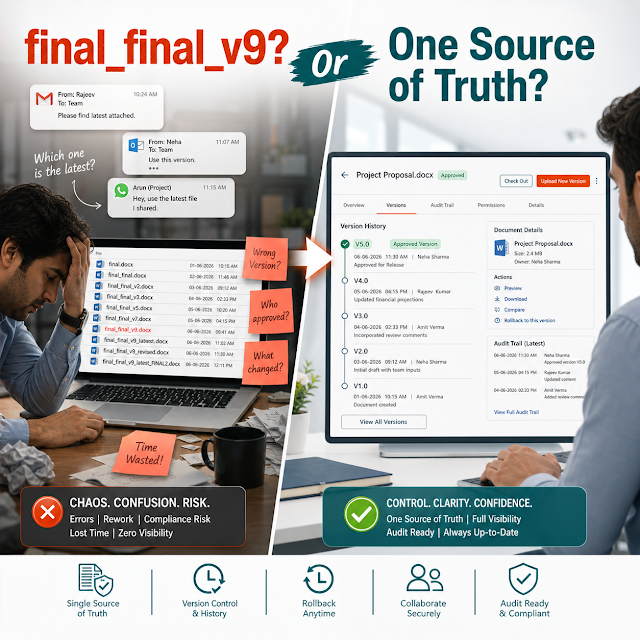

Yet in many banking environments, documents still live across email threads, shared drives, branch desktops, legacy imaging systems, physical files, and multiple line-of-business applications. This fragmentation creates a predictable outcome: delays during audits, inconsistent version control, unclear ownership, increased operational risk, and avoidable costs. When regulators ask “show me the trail,” teams scramble.

Modern document management for banks is not only about digitizing paper—it is about building a governed, searchable, secure, auditable content backbone that keeps compliance and operations aligned while enabling faster customer service and scalable growth.

Why this matters today

Banking operations are under pressure from multiple directions at once: rising customer expectations for instant processing, increased regulatory scrutiny, expanding cyber threats, and intense competition from digital-first players. Meanwhile, teams are asked to do more with less—without compromising on controls.

Document-related bottlenecks are often the hidden reason why onboarding takes days instead of minutes, why loan disbursement slips, why reconciliation requires manual follow-ups, or why exceptions pile up in back-office queues. In a regulated industry, “slow” is not just an inconvenience—it becomes a risk.

Decision-maker takeaway

A bank-grade document management system (DMS) is a control layer. It reduces compliance exposure, accelerates audit response, improves operational throughput, and creates a foundation for AI-driven search and automation—without sacrificing governance.

Key challenges banks face (and why they persist)

Fragmented repositories

Documents spread across shared drives, email, physical files, and product systems make it hard to find the “single source of truth.”

Manual KYC and onboarding trails

Teams collect, rename, and email files, creating inconsistent indexing and missing artifacts when auditors ask for evidence.

Weak version control

Multiple versions of policies, credit notes, and contracts lead to approval confusion and compliance gaps.

Audit response delays

Without audit-ready trails and structured metadata, collecting evidence is time-consuming and error-prone.

Access control complexity

Banks need least-privilege access by role, branch, product, and customer sensitivity—hard to enforce on shared storage.

Retention and legal hold gaps

Retention schedules, purge rules, and legal holds often depend on manual discipline—introducing inconsistency.

What’s at risk when document control is weak

Operational + Compliance risk isn’t hypothetical

Regulatory findings due to incomplete KYC evidence or missing approval trails

Audit exceptions caused by unverifiable document history, uncontrolled edits, or unclear sign-offs

Data leakage from excessive access privileges, unmanaged sharing, or shadow repositories

Customer dissatisfaction due to repeated document requests and long turnaround times

Higher operational costs from manual filing, retrieval, and rework across departments

For CTOs and Compliance Heads, the core question becomes: “Can we prove who did what, when, and why—at scale?” A modern DMS makes that provable.

Deep-dive: What “bank-grade” document management actually means

Banking document management goes beyond a repository. It must support governance, security, traceability, and process performance. In practice, this means the system should behave like an operational control plane for documents.

1) Structured metadata + content intelligence

Documents must be searchable not just by filename but by customer, account, branch, product, date range, document type, and case context. OCR and indexing transform scanned paperwork into searchable content. Well-designed metadata reduces retrieval time and prevents “orphan” documents that cannot be tied to a process.

2) End-to-end audit trails and immutable evidence

Auditors need proof of control: uploads, downloads, views, edits, approvals, and deletions—mapped to user identity and timestamps. For sensitive workflows (e.g., credit approvals, policy changes), banks often need tamper-evident logs and clear version lineage.

3) Role-based access control aligned to banking realities

Access must align to org structure and controls: maker-checker, branch-based permissions, segregation of duties, and restricted access for high-risk documents (e.g., PII, financial statements, legal opinions). Least privilege must be enforceable and auditable.

4) Workflow automation with SLA visibility

A DMS becomes valuable when it reduces cycle time: route documents for review/approval, trigger notifications, enforce mandatory fields, and show bottlenecks. Operations Heads benefit from measurable throughput and SLA compliance rather than “inbox-driven” work.

5) Records retention + defensible deletion

Banks must retain certain records for required durations and dispose of them when appropriate. This is both a compliance requirement and a security best practice—because “keeping everything forever” increases breach exposure and discovery scope.

The difference between “storage” and “enterprise document management” is measurable: retrieval time, audit response time, process cycle time, exception rates, and risk exposure.

A practical solution approach for banking leaders

A successful banking DMS initiative balances governance and adoption. If it’s too rigid, frontline teams bypass it. If it’s too loose, compliance fails. The right approach is phased, use-case driven, and measurable.

Start with high-risk, high-volume processes (KYC, account opening, loan documentation, audit responses) where control and speed both matter.

Define a metadata model that matches banking queries: customer ID, CIF, account number, product, branch, document type, and lifecycle stage.

Implement maker-checker workflows with mandatory checklists to reduce exceptions and rework.

Enforce least-privilege access with role-based controls and audit logs, aligned to segregation of duties.

Measure outcomes (TAT, SLA adherence, audit evidence time, exception rates) and expand to additional departments.

Feature breakdown: What to look for in a banking DMS

Centralized repository

A controlled, searchable source of truth for customer, operational, and governance documents with consistent structure.

OCR + intelligent indexing

Convert scans into searchable content, reduce manual tagging, and speed up retrieval for audits and customer requests.

Version control

Track changes, approvals, and document lineage so teams always work on the latest approved version.

Audit trail & activity logs

Prove access and actions across the lifecycle—critical for internal audit, compliance testing, and regulator queries.

Role-based access control (RBAC)

Granular permissions by role, branch, department, and document sensitivity to reduce exposure and enforce segregation of duties.

Workflow automation

Maker-checker approvals, task routing, reminders, escalations, and SLA visibility to reduce cycle time and errors.

Retention & disposal policy

Rule-based retention and defensible deletion that aligns with records obligations and reduces long-term risk.

Secure sharing & controlled access

Enable secure sharing with internal stakeholders and auditors while maintaining strong access governance and traceability.

Traditional document handling vs modern banking DMS

Traditional approach

Storage: Shared drives, email, local folders

Search: Filename-based, dependent on tribal knowledge

Risk: Least privilege, logs, policy-based retention

Banking use cases that benefit immediately

KYC onboarding & customer due diligence

Centralize identity proofs, address verification, risk assessments, and approvals. Reduce repeat document requests and ensure evidence completeness during reviews.

Scenario: A relationship manager uploads customer documents, compliance reviews them in a controlled queue, and the final decision is stored with timestamps and rationale—ready for audit.

Loan origination & credit documentation

Manage financial statements, collateral documents, valuation reports, sanction letters, and approvals with strict versioning and maker-checker controls.

Scenario: Credit teams retrieve complete loan files in seconds for portfolio reviews, reducing turnaround time and improving disbursement predictability.

Internal audit & compliance testing

Provide structured evidence packs with audit trails, document histories, and access logs—without disrupting operations.

Scenario: When auditors request samples, the bank generates case-based exports with metadata, approvals, and activity logs—cutting weeks of manual effort.

Policies, SOPs, and governance documents

Ensure employees always reference the latest approved policy, with acknowledgments and a clear history of changes and approvals.

Scenario: Compliance updates a policy; the system routes it for approval, publishes the new version, and retains older versions for regulatory traceability.

Vendor management & procurement

Control contracts, NDAs, due diligence checklists, renewal alerts, and approval trails—reducing vendor risk and missed renewals.

Scenario: Finance and procurement get renewal reminders; legal sees only relevant contract folders; audit can validate approvals and exceptions.

Customer service & dispute handling

Reduce resolution time by giving agents quick access to communication history, forms, and supporting documents—without overexposing sensitive data.

Scenario: Dispute teams retrieve the complete case file, ensuring consistent responses and strong evidence if escalated.

Implementation perspective: How to roll this out without disruption

Banking leaders typically worry about two things during DMS modernization: operational disruption and control gaps during migration. Both are manageable with a phased plan and clear governance.

Apply OCR for scanned documents and automate routing for approvals and exceptions. Add SLA tracking and dashboards for operations leadership.

Phase 3: Integrate and scale

Integrate with existing banking applications as needed, expand to additional departments, and refine governance as usage grows.

What decision-makers should demand from the rollout

Clear ownership (Compliance + Ops + IT) and defined success metrics

Controlled migration plan (what moves, what stays, what gets retired)

Change management for branch teams and back-office users

Evidence that audit trails, retention, and access control are working as designed

Business impact and ROI: Where the gains show up

A banking DMS is often justified as a compliance initiative, but the strongest ROI usually comes from operational efficiency and reduced rework—especially in high-volume document journeys like onboarding and lending.

Faster processing and shorter TAT

Standardized capture, automated routing, and instant retrieval reduce turnaround time for onboarding, renewals, and loan disbursement.

Lower audit effort and disruption

Evidence packs, audit trails, and metadata-based retrieval can cut weeks of manual compilation and reduce business disruption during audits.

Reduced risk exposure

Least-privilege access, controlled sharing, and retention policies reduce the chance and blast radius of document leaks.

Better customer experience

Fewer repeat document requests, faster resolution, and consistent case context improve trust—critical in competitive banking markets.

ROI framing for Finance Heads

Model value across: (1) reduced manual hours spent searching/compiling documents, (2) reduced rework from missing/incorrect documents, (3) faster revenue realization from quicker onboarding/loan disbursal, and (4) risk reduction from fewer audit findings and improved control evidence.

Future readiness: AI search and automation—without losing control

AI in banking content management is only as good as the underlying governance. If documents are scattered, inconsistently tagged, and poorly secured, AI makes results faster—but not necessarily correct or safe. The right DMS prepares your bank for AI responsibly.

How AI-ready document management helps

Smarter search: find documents by meaning and context (customer, product, case) rather than exact filenames.

Faster classification: auto-suggest document types and metadata to reduce manual tagging errors.

Exception detection: flag missing mandatory documents or inconsistent fields early in the workflow.

Summarization for reviewers: help compliance and credit teams quickly understand long documents while keeping the original evidence intact.

Governance note for Compliance and Risk teams

AI capabilities must respect access control boundaries. A governed DMS ensures AI search results only reveal what a user is permitted to see, and that every access remains logged—supporting responsible AI adoption.

FAQs

1) Is a document management system the same as ECM in banking?

DMS typically focuses on storing, organizing, and controlling documents. ECM (Enterprise Content Management) extends this with broader governance, workflows, records management, and enterprise-wide integration. Many banks use DMS capabilities as a foundation and scale into ECM maturity.

2) How does a DMS help with audit and compliance?

It centralizes evidence, enforces controlled access, captures version history, and provides audit trails showing who accessed or approved documents and when. This reduces audit response time and improves defensibility of controls.

3) What banking workflows benefit most from automation?

High-volume processes with clear checkpoints: KYC onboarding, loan processing, renewals, exception handling, vendor due diligence, and audit evidence collection. Automation reduces delays, rework, and handoff confusion.

4) How do we ensure document security without slowing users down?

Use role-based access control aligned to job functions (plus segregation of duties), apply consistent metadata, and provide fast search so users don’t create shadow copies. Security improves when the official system is the easiest system to use.

5) What should leadership measure to confirm success?

Track turnaround time (TAT), SLA adherence, exception rates, audit evidence retrieval time, and access policy violations. These metrics show whether the DMS is improving both performance and control.

Ready to modernize banking document control—without compromising compliance?

If your teams are spending too much time searching for documents, compiling audit evidence, or managing approvals via email, it may be time to shift to a governed document management and workflow automation approach designed for banking realities.

Explore ShareDocs DMS to strengthen compliance readiness, improve operational turnaround, and build an AI-ready foundation for secure enterprise search and automation.